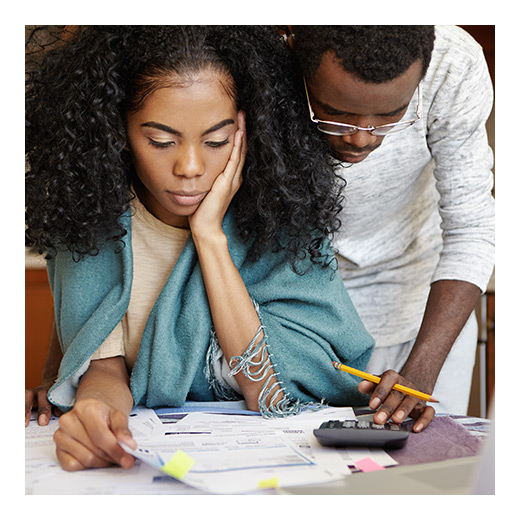

Making a Budget Worksheet for Your Apartment

Moving out on your own for the first time can be stressful. There are a lot of things you need to learn to juggle, including budgets. When you first rent an apartment forming a budget for food, rent, utilities, and more can seem like a daunting task. That is why creating a budget worksheet is a great idea. By creating a budget worksheet you can get down on paper what you expect your monthly expenses will be compared to your income. It helps you keep track of your finances and even prepare for any surprises.

Three Budgeting Principles

When creating a budget worksheet there are three principles you’re looking for: You want to understand where your money is going each month, you want to get a foundation for how to save more and spend less, and you want to be able to get control of your money. These three principles will help you get an idea of where you are currently and where you would like to go.

Mark Your Income

It is never a good idea to spend more money than you have, so figuring out your income is the first step. If you have a steady job this can be an easy part, as you likely have a set income each month. If you have some side jobs in the gig economy some months can be better than others, but you can take that into account. For example: If you earn extra money shoveling snow on the side you’re going to have more income in January as opposed to June. Be sure to use your best judgement.

Figure Your Expenses

Some of these will be easier than others. Your rent is going to be static for each month of your lease. The same is true for a car payment, student loan, or anything else. Utilities will vary, but not by much. Where you really start to see your budget is in your variable expenses. What do you spend each month on eating out or going out to bars? How much do you spend on entertainment? It is these variable expenses that can be cut if necessary.

Figure Out Your Goals

Do you want to save more? Then write down a specific dollar amount you want to save each month and consider it an expense. You can even start a savings account and set up an automatic draft from checking for a certain amount each month, or even each week. Time it with when your paycheck arrives so that you know you will have the money there to save. Be sure to check on your spending each week and adjust as needed.

With these tips it is easy to get a handle on your finances and see where some sacrifices (if any) need to be made. You can even purchase budgeting programs such as Quicken that will show you where your money is going over time.